Norbert Lou: The Best Investor That No One Talks About

The Unknown Man Behind the World's Most Selective Hedge Fund

"To this day, I hand out the first 3 write-ups he wrote on the Value Investors Club to my students at Columbia, to show them what a brilliant, concise, straightforward and clear investment thesis looks like." - Joel Greenblatt

Norbert Lou is a name that might not ring a bell for most people. Despite managing perhaps the world's most selective hedge fund for over 20 years, there's very little public information on him. If you google "Norbert Lou", you won't find pictures, you won't find interviews (except for one), and you won't find any investor letters.

So how did this relatively unknown individual come to manage more than $300 million in assets from some of the world's most respected investors?

Discovering NVR

In his post college years, Lou worked as an analyst at a small investment shop named Brown Brothers Harriman then later accepted a position at the activist investing firm Elliott Management. During those years, Lou began to form an idea of the investing style that he liked.

Despite witnessing the success of Elliott's active investing approach, in his one public interview with Santangel's Review, Lou stated "it didn't really suit my nature." Instead, Lou preferred to search for companies where he could sit by passively and watch the business generate extraordinary returns on the capital for long periods of time.

Insert NVR.

NVR was a homebuilder. However, unlike traditional homebuilders which would acquire large plots of land and hold it on their balance sheet while they developed homes on it, NVR would instead purchase an "option" on the land. This meant that NVR would usually pay 5%-7% of the land value upfront and then could exercise the right to pay the remainder once the lot was finished. This model kept the inventory off of NVR's balance sheet, which helped the company during market downturns.

Lou first discovered and invested in NVR in 1997 while managing his own personal money along with his mother's retirement. At the time, NVR was trading for roughly $23 per share. Today, the stock trades for just over $7,000 per share.

Ironically, Lou first decided to take a look at NVR because the company announced a large buyback program. However, he quickly discovered that the company had much better uses for its capital. In fact, this helped Lou solidify what he looked for in prospective investments. He describes it this way "You actually want the companies that have such bountiful reinvestment opportunities that they don’t buy back any shares".

Founding Punch Card

In 2001, after nearly a decade successfully investing him and his mother's own money, Lou came across an exclusive, members-only investing forum called Value Investor's Club.

Lou applied to the club with a write-up on NVR under the pseudonym "Charlie479". His application was accepted and Lou followed his initial write-up with two other investments that both handily outperformed the market.

This caught the attention of the club's founders Joel Greenblatt and John Petry, who ran a fund of funds called Gotham Asset Management. The two were so blown away by the write-ups that they invited Lout to meet in person and encouraged him to start a fund of his own with seed capital from Gotham.

Inspired by Warren Buffett's punch card analogy, he decided to name the firm Punch Card Management.

“I always tell students in business school they’d be better off when they got out of business school to have a punch card with 20 punches on it. And every time they made an investment decision, they used up one of their punches, because they aren’t going to get 20 great ideas in their lifetime. They’re going to get five or three or seven, and you can get rich off five or three or seven. But what you can’t get rich doing is trying to get one every day.” - Warren Buffett

Performance & Holdings

While Lou doesn't publicly disclose the fund's performance on a regular basis, there is some data that we can parse together.

While managing him and his mother's own money from 1994 to 2003, Lou calculated that he had generated annual returns of 38.5%!

From the inception of his fund in 2004 to his one public interview in 2011, Lou's fund returned 14.5% a year net of fees. That also came during a time period when the S&P 500 returned just 2.2% a year. So while we don't know his performance over the last decade, we can say confidently that he crushed the market for at least 17 years.

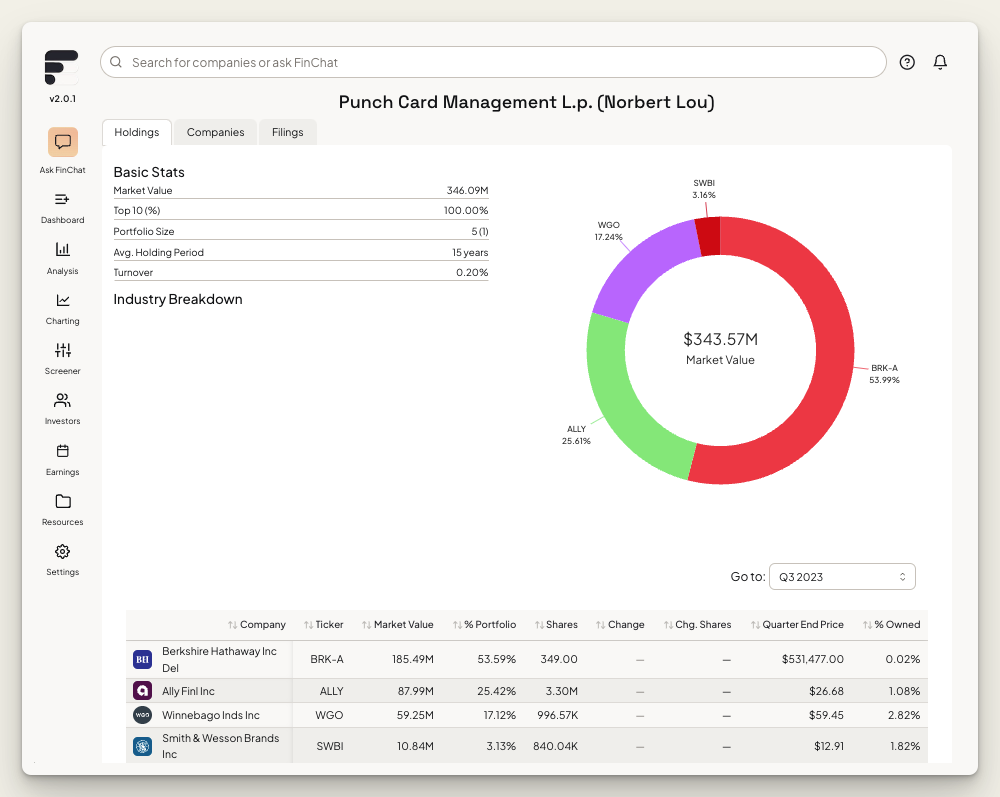

Fortunately for individual investors, even though a fund's performance isn't required to be reported, any fund with more than $100 million in assets must publicly disclose its holdings. And for Punch Card Management, there are currently just 4:

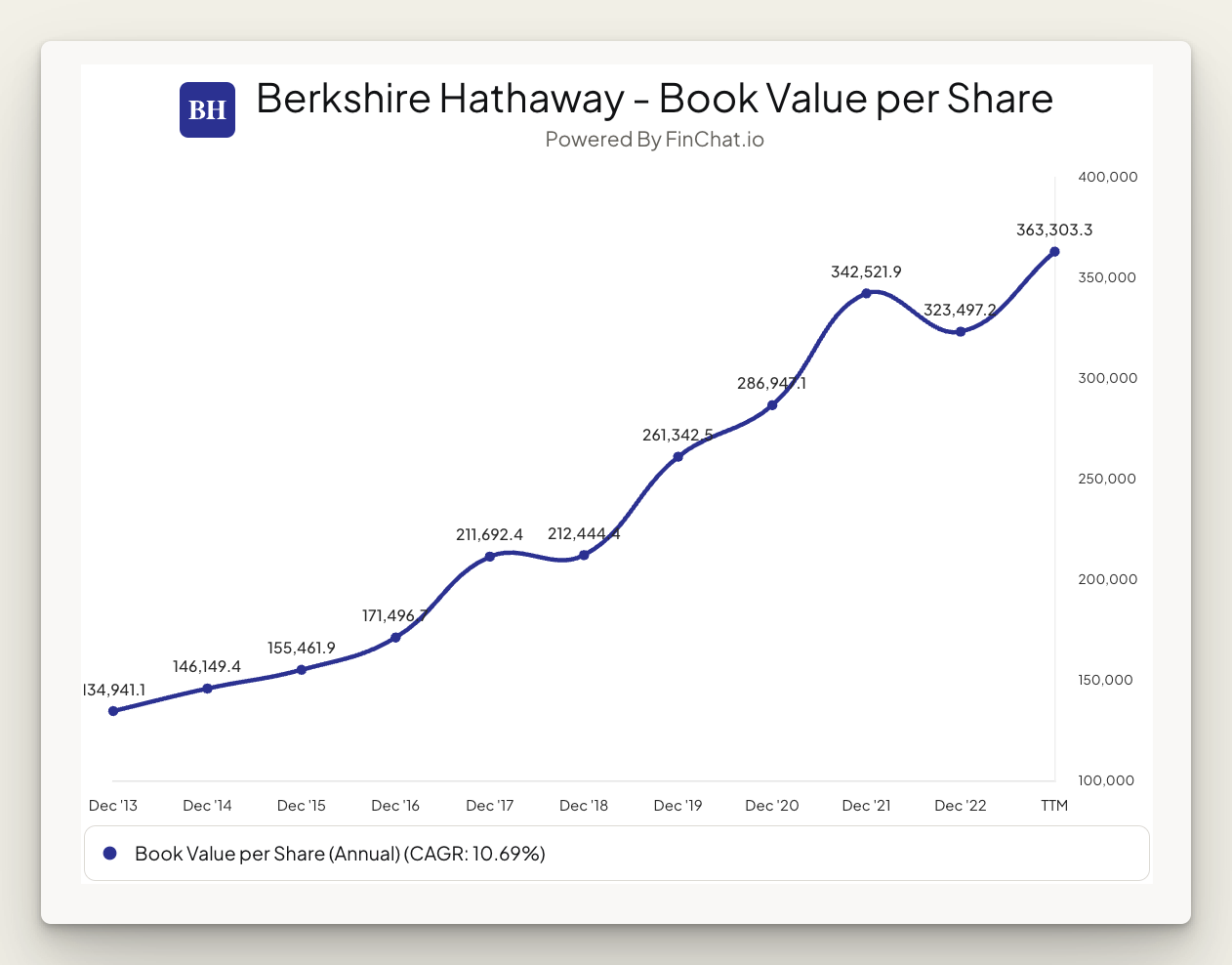

Berkshire Hathaway:

Lou fell into owning Berkshire Hathaway (NYSE: BRK.A) by first investing in Burlington Northern Santa Fe (BNSF) in 2009. However, less than a year later, it was announced that his new investment was being acquired by one of his own investing role models, Warren Buffett.

When Berkshire Hathaway acquired BNSF in 2010 for $26 billion., current BNSF shareholders were given the option to either take cash or convert their holdings into Berkshire shares. Lou elected to take the Berkshire shares.

While many people frown upon fund manager's buying Berkshire since it seemingly defers the capital allocation skills to Warren Buffett, Lou saw it differently. At the time, he thought Berkshire was actually quite undervalued and he's chosen to hold his shares ever since. As of his latest 13-F filing, Berkshire shares accounted for 54% of Punch Card's portfolio. So far, that's a bet that has worked out quite well.

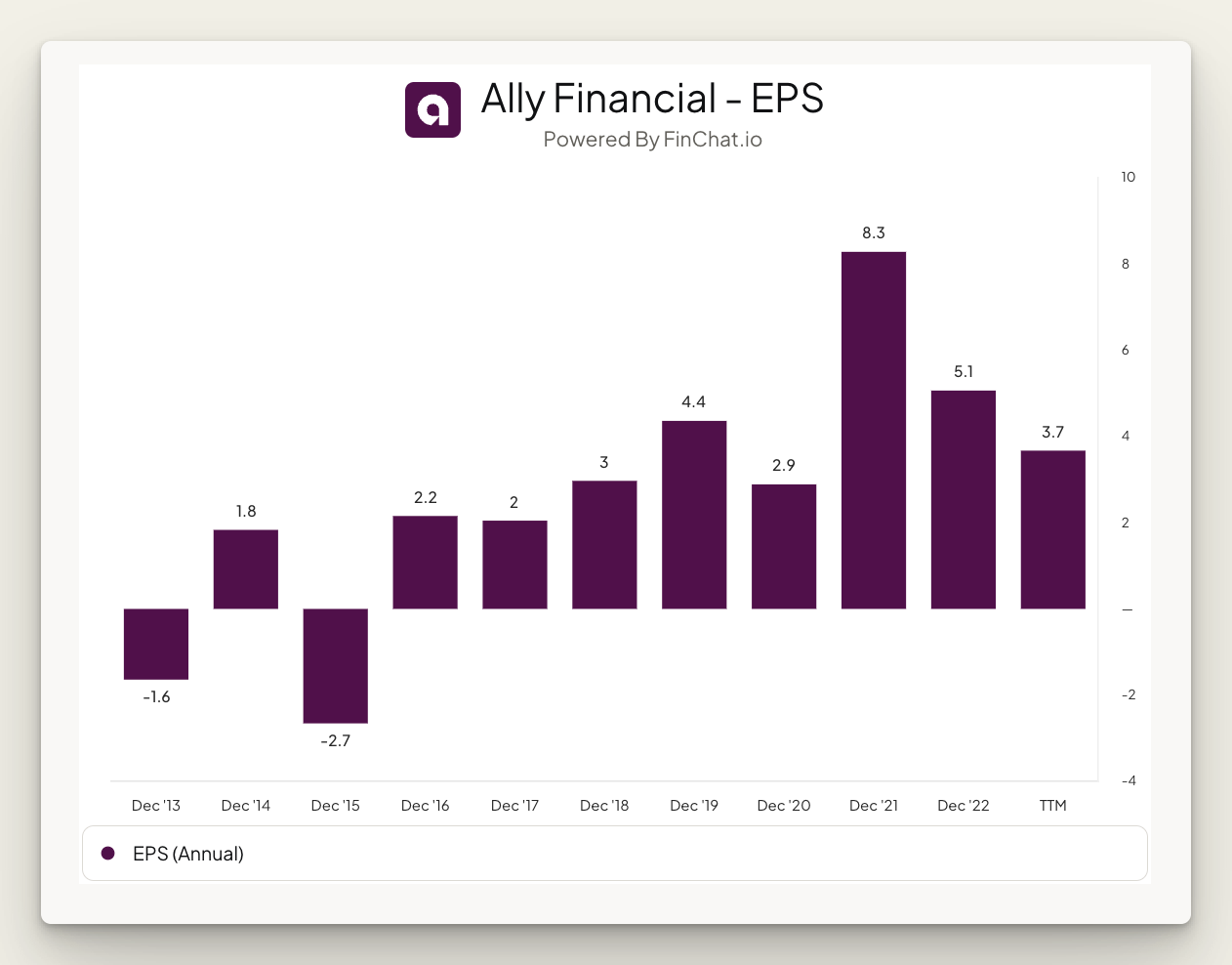

Ally Financial

According to FinChat.io, which tracks the portfolio changes of Super Investors like Norbert Lou, Punch Card first took a stake in Ally Financial (NYSE: ALLY) during the first quarter of 2020.

Ally is the largest digital-only consumer bank in the US. Thanks to its low-cost, no branch model Ally is able to pass through its cost savings to consumers in the form of higher interest rates on savings accounts. This has helped the bank to amass a retail depositor base of 3 million people, ~4x larger than a decade ago.

Ally is using these customer deposits primarily to finance its automotive loans. Prior to the great financial crisis, Ally was the financing arm of General Motors so it has decades of experience originating car loans.

Given the cost advantages of Ally's model and the fact that the stock trades at a P/E of 9x on depressed earnings, it isn't too surprising to see this account for 25% of Lou's portfolio.

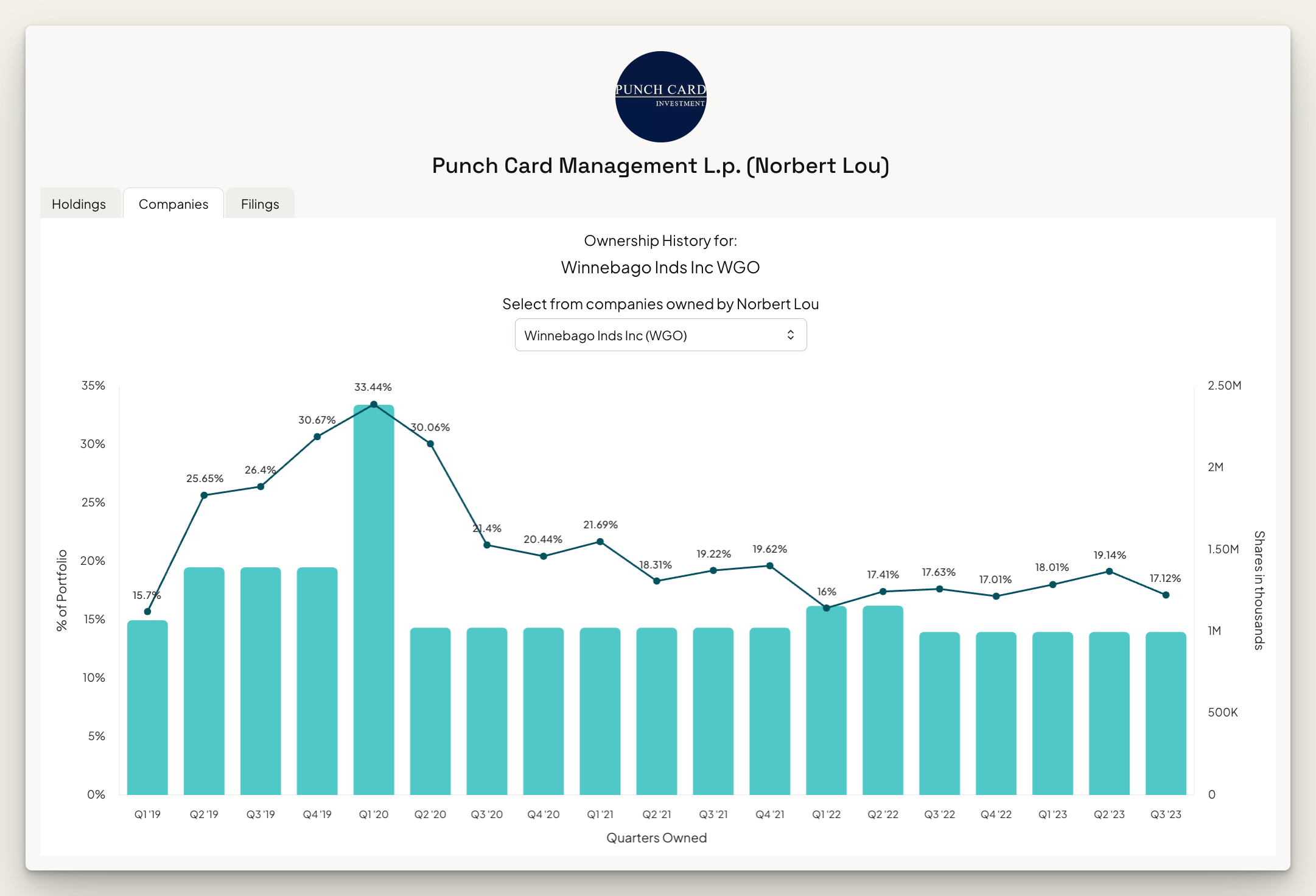

Winnebago Industries

Winnebago Industries (NYSE: WBGO) is the largest manufacturer of towable RV's and motorhomes in the North America. While it has been a core holding for Punch Card since 2019, Lou seems to have a rocky past with the company's management team.

In March of 2020, Lou filed a 13D announcing that he controlled more than 5% of the company. Accompanied to the 13D, Lou wrote a letter to Winnebago's board of directors advocating for the reduction of debt and raising concerns about excessive executive compensation at a time when lower-level employees were being let-go.

Following the letter, it seems not much changed, and Lou sold down his ownership to below 5%. Today it remains 17% of the Punch Card portfolio and Winnebago's stock has appreciated considerably since Lou's initial purchase.

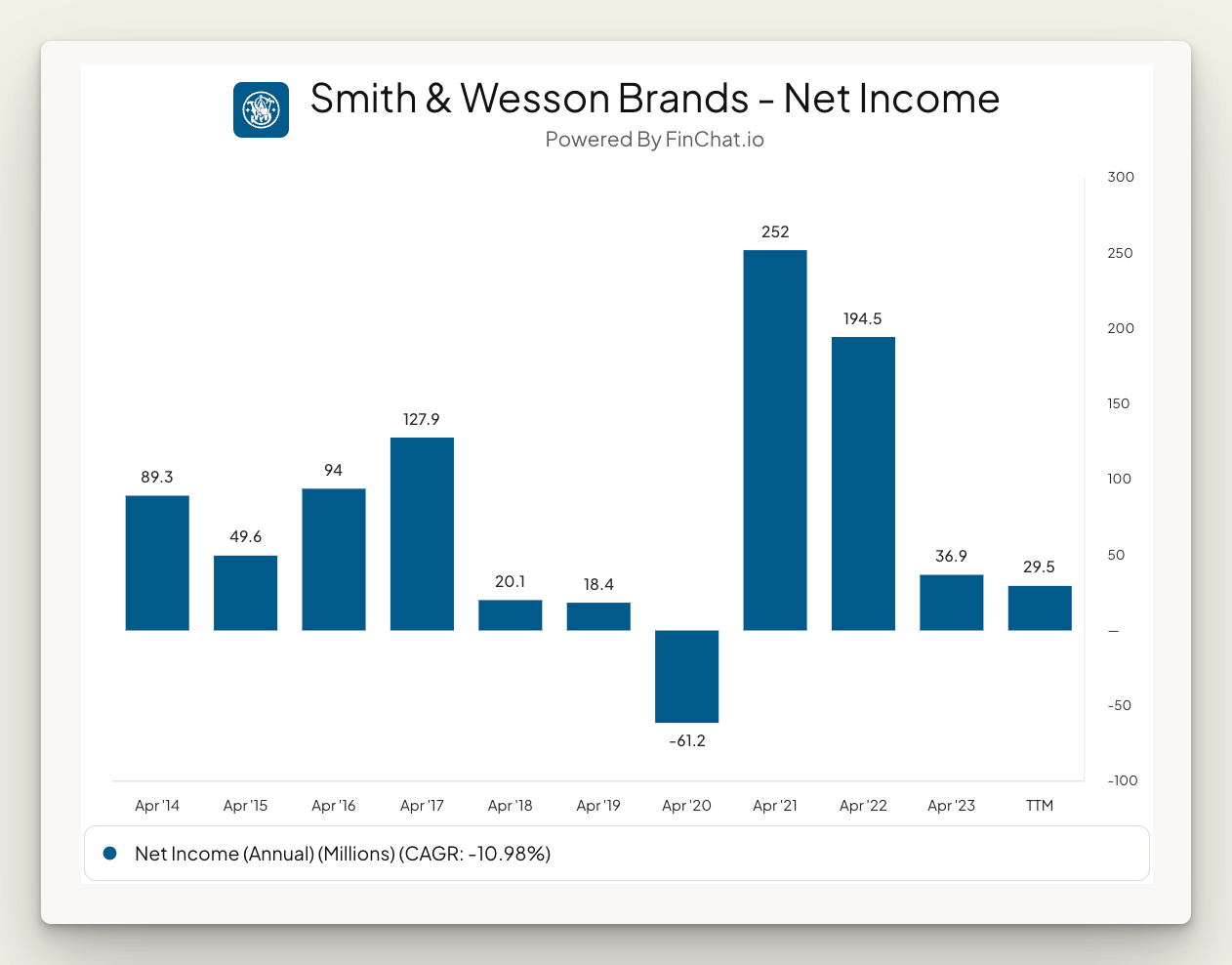

Smith & Wesson Brands

Norbert Lou first bought Smith & Wesson Brands (NASDAQ: SWBI) in Q2 2022. Smith & Wesson is one of the leading firearm manufacturers and has been around since before the civil war.

Smith and Wesson is a beloved and well respected brand by firearm enthusiasts and has strong relationships with its network of retail partners. Due to a recent inventory build-up and being forced to relocate their main manufacturing facility, cash flow has declined sharply for the business.

However, for investors that believe Smith & Wesson can return to its previous earnings power of ~$200 million annually, the stock looks cheap here with the company's current enterprise value hovering around $670 million.

While the brand has certainly proven to be durable, and the stock could have some serious upside if things go right, Lou doesn't seem confident enough to make this a core holding. For now it remains just 3% of the Punch Card portfolio.